Credit burndown pricing has become more common, especially in AI and compute-heavy SaaS products. According to Growth Unhinged, credit model adoption grew 126% year over year in 2025.

Credit burndown is popular because it pulls many different usage types into one balance. Customers prepay for a pool of credits and spend them across different features. This gives them better control over their budget.

A credit burndown model also supports flexible SaaS pricing. Product teams can easily adjust how many credits an action costs without changing the entire pricing infrastructure.

In this article, we'll explain what credit burndown means, why it's useful, and how to implement it in your product.

Credit burndown is a usage-based pricing model where customers prepay for credits that burn down as they use your product.

It works by assigning a credit cost to each action, with all usage deducted from a single credit pool.

Credit burndown is useful if usage varies significantly between customers. It simplifies pricing for users while giving SaaS teams the flexibility to adjust burn rates and pricing.

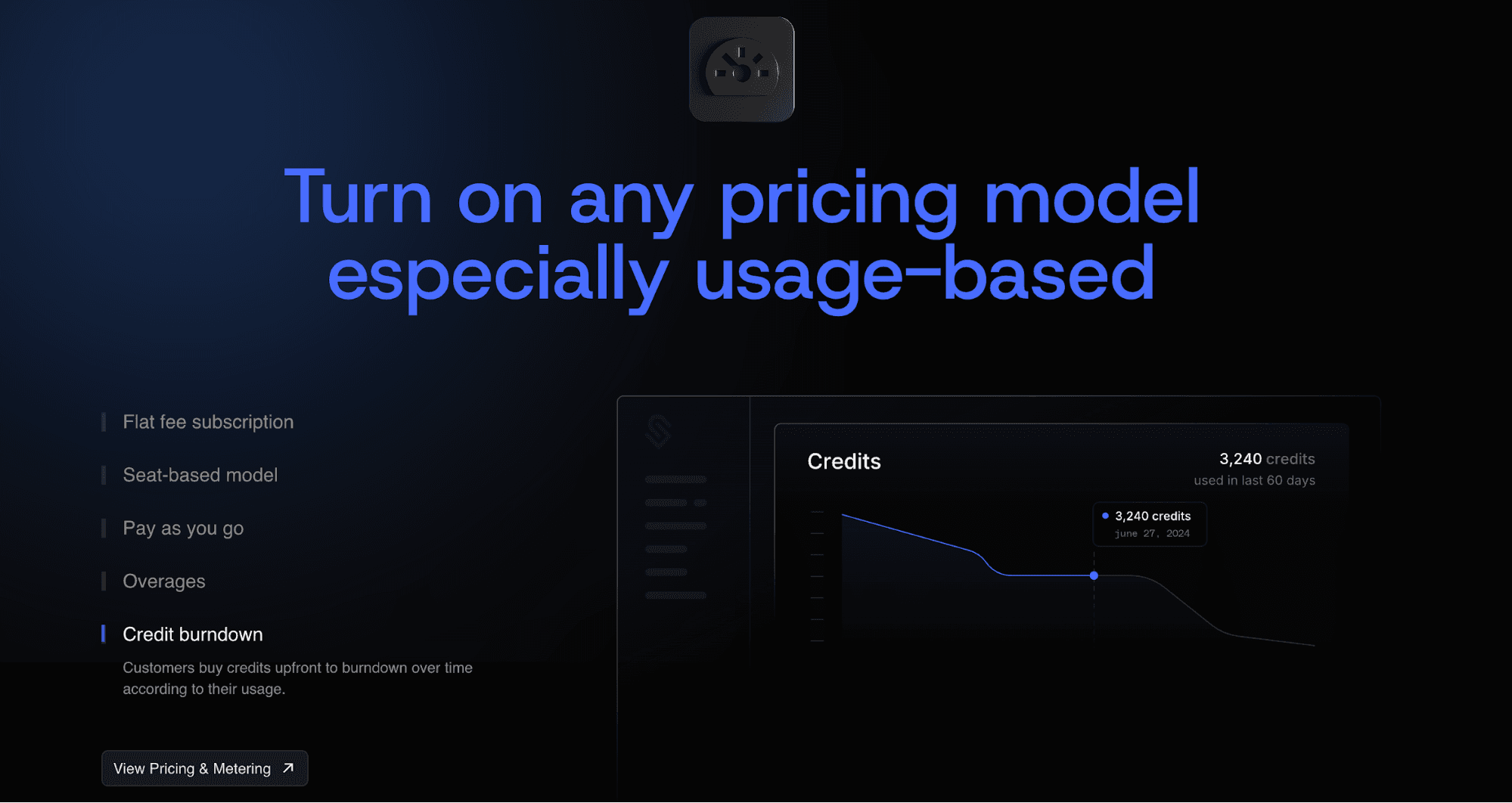

Schematic can ship any pricing model, including credit burndown, without billing rebuilds. This allows SaaS businesses to continuously iterate on monetization.

Credit burndown is a usage-based pricing model that prices the outcome the user wants, not the technical inputs.

Users see a single credit cost per action aligned to outcomes they care about. Technical details, such as API calls, compute time, and AI models, remain internal.

The set price per action provides clarity and predictability. Customers maintain a prepaid credit balance that decreases with each billable action (e.g., model calls, file processing, or exports).

Credit burndown allows SaaS companies to group multiple features, actions, or services under one pricing system.

For customers, this means one balance funds everything they do. Model runs, file processing, call transcription, enrichment, exports, and reports all share a common credit pool of usage.

For example, an AI enrichment might cost one credit, a call transcription consumes five credits, and a long video transcode uses 10 credits.

The credit burndown pricing model works by giving customers a credit balance that burns down as they use your product.

Customers pre-purchase credits or subscribe to a plan with a set number of credits.

As users take actions, such as making an API call or accessing an AI feature, credits are deducted from that balance. All usage pulls from a single pool, even if different actions have different credit values.

Then, the model tracks the customer's usage in real time to ensure accurate billing.

When the credit balance runs low, customers can purchase additional credits or upgrade to a subscription plan with more credits. They can enable automatic top-ups to avoid usage interruptions.

Bundles are also a natural place to add volume discounts or promotional credit prices.

Credits are typically tied to a billing period. In most cases, unused credits expire at the end of each billing cycle, whether monthly or annual.

Credit burndown reduces complexity for users and increases flexibility for your team. Instead of exposing technical details, it turns usage into a simple and value-based system.

Customers see one balance and a clear cost per action. They can make informed decisions and keep spend predictable.

Your team benefits from clear usage limits, so you can adjust burn rates and credit prices without breaking trust. That combination helps startups find their price and gives established products a clean bridge from product-led growth to enterprise.

Credit burndown pricing can also support customers throughout the customer lifecycle, from initial adoption to expansion and upselling.

Credit burndown pricing is useful if customers keep asking “what will this cost me?” or your team avoids pricing changes because your current model is too brittle.

Credit burndown shows up across many usage-based products. Regardless of the category, the pattern stays the same: different actions are grouped into a single pricing metric and consume credits from one balance.

The examples below show how credit burndown simplifies the buyer’s decision and gives your team room to experiment without changing what you sell.

In an AI product, users might summarize a document, create a blog post, or synthesize a multi-file report. These actions might cost 1, 5, or 10 AI credits, respectively.

Users see clear per-action costs in line with the goals they want to accomplish. Behind the scenes, your team manages the pricing models and prompts.

For an email verification platform, marketers might upload lists to validate emails and prepare marketing campaigns.

One credit might cover 100 email validations, while a pre-send spam test on the campaign may cost 3 credits. Regardless of provider changes or retry rates, the buyer watches one balance.

Some companies may also consider freemium pricing. They offer basic email validation features for free to attract users and upsell advanced capabilities.

Adding captions might consume 5 credits per minute in a video podcast editing product. Meanwhile, improving audio automatically could cost 15 credits per minute.

Creators can estimate costs up front and avoid surprise invoices.

For a data enrichment product, users might spend 1 credit to request an updated company profile and 5 credits to find phone numbers associated with an email address.

Users stay focused on the information they are looking up without thinking about which dataset powers the result.

Some companies may use value-based pricing to set credit costs based on the perceived value of the data provided.

Here's how you can set up a credit burndown model.

Decide what one credit represents in your product. Assign a credit cost to each action based on effort, infrastructure cost, or value delivered.

Keep the system easy to understand so customers can estimate their spending.

In some cases, you may introduce multiple credit types if your product offers different plans, such as basic vs. premium.

However, most companies start with one credit type to keep usage-based billing simple.

Build a system that tracks every action tied to credit consumption.

When a user performs an action, the system should log it and deduct the correct number of credits.

Accuracy matters here. If tracking is off, customer trust breaks quickly.

Over time, it will generate usage data that helps you understand how customers interact with your product. This enables you to make smarter SaaS pricing and packaging decisions.

Give customers a clear view of their credit balance, activity, and billing information.

Highlight trends so users can understand their usage patterns over time. This helps them plan usage and avoid surprises.

Keep the interface simple and intuitive. Customers should be able to check their remaining balance and understand usage in seconds. This builds trust and reduces support requests.

Decide how credits behave over time. Some companies set expiration dates tied to a billing cycle, while others allow unused credits to roll over.

Make this decision on your business model and how customers use the product. If usage varies month to month, credit rollovers can support a better customer experience. If not, expiring credits can help drive consistent usage.

Make these rules clear upfront. Customers should know exactly how long their credits last and how that affects their spending.

Explain how credits work on your pricing page, onboarding materials, and product UI. Show examples of usage and costs.

Show how different actions translate into credit consumption and provide examples based on real-world scenarios.

Use simple language so customers understand how they will be charged. Clear communication helps them feel confident and reduces friction once they scale usage.

Schematic helps you launch and manage any pricing model, including credit burndown, without hard-coded logic.

Schematic, built on Stripe, serves as the system of record for your product catalog, plans, credits, software entitlements, limits, and exceptions. Stripe handles payment transactions and sales invoices, while Schematic enforces access in-product at runtime.

With Schematic, you can ship credit burndown pricing in days, not months. You define credit value, assign it to features, and track usage automatically.

Schematic also provides drag-and-drop billing components, such as customer portals and usage dashboards. Customers can see their credit usage clearly, while your team retains full control over pricing and packaging decisions.

Engineering stops maintaining the billing and entitlement code. Product teams can continuously iterate on monetization.

The credit burndown model is a usage-based billing approach where customers pay for credits upfront that burn down as they use your product. It uses credit values as a universal metric to simplify billing across different product features.

Credit burndown groups all usage into one trackable unit, while traditional usage-based pricing charges directly per metric. Credit burndown is useful for multiple billable actions or model tiers. Traditional pay-as-you-go makes sense if you only have a single feature that requires tracking.

Customers track credit usage through dashboards or customer portals. These tools show remaining credits, recent activity, and usage patterns. They help users understand spending and avoid billing surprises.